11. September 2019 | Establishments and the Demand for Personnel

Working time accounts in the public- and private sector: flexible working hours are becoming increasingly important

Both employers and employees can benefit from working time accounts, depending on their configuration. Working time accounts offer employers a tool for adapting the work-input according to demand without hiring or dismissing staff. This saves companies recruitment and training costs as well as costs associated with dismissal.

In international comparison Germany is considered as an economy which relies more on internal than on external flexibility when dealing with fluctuations in demand. This feature of the German labour market is mainly attributed to the institutional setting with strong job security regulations but also to the special and sustainable way German firms train and keep their skilled workforce.

In addition to the job-stability generated by working time accounts, employees can profit from them where they facilitate a better reconciliation between work and family life. This applies in particular to so-called short-term accounts. These are accounts in which the balances (i.e. working-time surpluses or deficits) have to be settled within a period of up to one year, or where they may not exceed a certain value by a certain date. This period is referred to as „compensation period“.

In addition, there are so-called separate long-term accounts (“Zeitwertkonten”). From the point of view of employees, these have the purpose of accruing time for longer periods of leave (sabbaticals) or enabling early retirement. Firms may offer such accounts in order to be more attractive to applicants.

Restrictions on the use of working time accounts

However, employees are rarely able to use working time accounts based purely on personal needs. On the contrary, it can be seen that the increased flexibility of working time is primarily geared towards the employer’s interests. This means that employees can use working time accounts for their own interests if this is compatible with the company’s requirements. Employees often have to agree on a planned reduction of working time credit with their superiors and colleagues in advance so that they do not conflict with the company’s needs. How employees set up and reduce working time credits depends in particular on the employer’s capacity utilisation.

Working time accounts were used particularly intensively in the Great Recession of 2008/2009 in order to reduce the working hours of employees temporarily as shown in a 2010 study by Joachim Möller. A 2014 analysis by Alexander Herzog-Stein and Ines Zapf explains that in this instance the use of this instrument helped delay or even avoid negative employment adjustments in times of crisis. The findings on the longer-term employment effects of working time accounts in the Great Recession are not uniform as a selection of studies show: Michael C. Burda and Jennifer Hunt (2011), Olga Bohachova, Bernhard Boockmann and Claudia Buch (2011), Enzo Weber (2015), Almut Balleer, Britta Gehrke and Christian Merkl (2017). However, there is no doubt that at least in the short term they helped to stabilize the employment level or provided companies with a breather as shown by the 2014 study by Alexander Herzog-Stein and Ines Zapf.

In the following sections, we use the data from the IAB Establishment Panel firstly to examine how the spread of working time accounts developed. We show differences according to company size and sectors. After a differentiated consideration of the compensation periods, we look for explanations as to why companies rarely use long-term accounts.

Development, distribution and design of working time accounts

More and more companies and administrations use working time accounts. Between 1999 and 2016, their share almost doubled from 18 percent to 35 percent. Likewise, more and more employees have a working time account: across all companies, their share has risen from 35 percent to 56 percent.

If one considers only companies and administrations with working time accounts, then the existing regulations apply to large sections of the workforce. In these companies, the share of employees with working time accounts increased from around 77 percent to around 87 percent between 1999 and 2016. Therefore, where companies are running working time accounts, almost nine out of ten employees can use them.

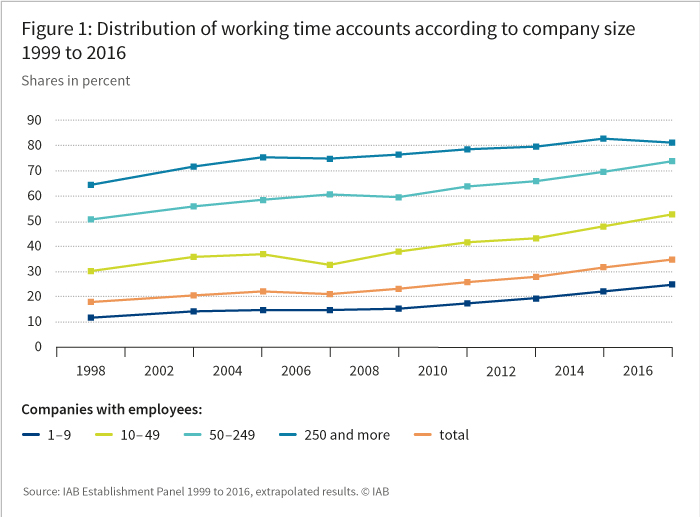

Working time accounts are especially widespread in larger companies

Working time accounts are significantly more widespread in larger companies than in smaller ones. Amongst the companies with 250 or more employees, the share was about 81 percent in 2016, whereas in small businesses with up to nine employees only around one in four companies had working time accounts. The overall increase in enterprises with working-time accounts since 1999 has been largely parallel in all the individual size categories (see Figure 1).

The proportion of employees with a working time account is also higher in larger companies than in smaller companies. In 2016, around 72 percent of those working in a company with at least 250 employees had working time accounts. In companies with up to nine employees, this figure was around 24 percent.

Public administration and social security administrations are most likely to have working time accounts

Working time accounts are also distributed very differently across sectors. They are most widespread in public- and social security administrations (76 % of enterprises and administrations), in energy, water, waste and mining (59 %) and in intermediate product industries (54 %). Working time accounts are clearly underrepresented amongst financial and insurance service providers (26 %) as well as in the hospitality sector (24 %). Thus, the share of employees with working time accounts is highest in public administration and social insurance (78 %) and lowest in the hotel and catering sector (34 %).

Shorter compensation periods dominate

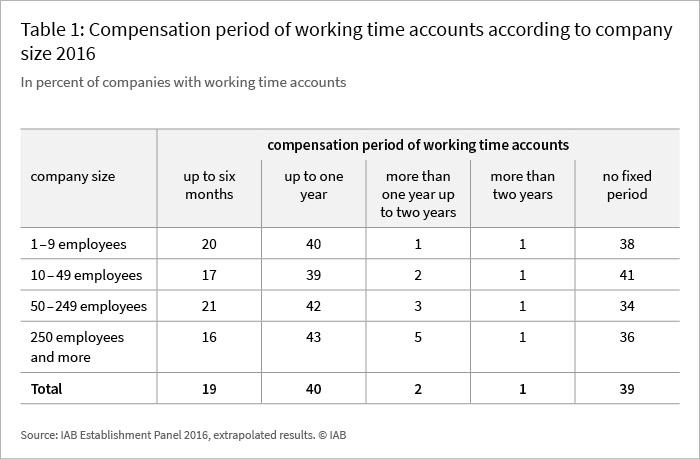

In four out of ten companies – and thus most companies with working time accounts – the compensation period is between half a year and one year (see Table 1). In every fifth firm there is a shorter time frame of up to half a year. Flexitime models with this relatively short compensation period provide a low flexibility potential, not only with regard to time credits and debts. Thus, an efficient adaptation of the labour force is limited. Seasonal as well as cyclical fluctuations can hardly be cushioned by such a short compensation period, which explains its lesser importance.

Many companies also have working time accounts without a fixed compensation period. These may be companies that do not regulate the compensation period at all. Or they may generally determine the length of the compensation period, but also adapt and vary these at short notice according to operational need. For example, collective bargaining agreements can provide for longer compensation periods if employees cannot reduce the accumulated time credits in the originally envisaged period due to high demand for products or services.

Working time accounts with a compensation period of more than one year are less widespread: in two percent of firms there are accounts with a time frame between one and two years, and in only one percent there is a compensation period of more than two years.

Long-term accounts are less widely used

Long-term accounts are designed to facilitate a life-time-oriented workforce design. Thus, accumulated (time) credit can be used, for example, for further training activities, for extended leave for family or other duties and interests, or early retirement.

With the introduction of the Law on Improving Flexible Working Hours (Flexi II Act) in 2009, the use of long-term accounts has been placed on a new legal footing. With this legal safeguard, the legislator wanted to give a strong boost to the distribution of long-term accounts of which until then little use was made.

Nevertheless, in 2016 just two percent of companies in Germany offer their employees separate long-term accounts and this value has changed little in the last 15 years.

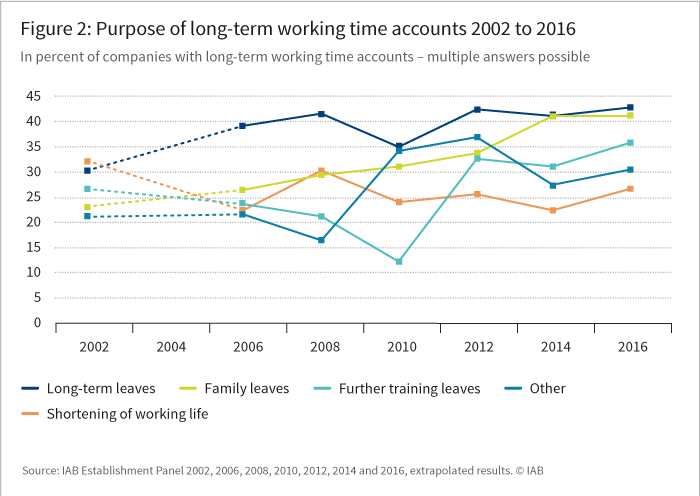

In terms of the purpose of long-term accounts, a distinction can be made between optional and age-related accounts. In the optional variant, the accumulated time credits are drawn on whilst the employee is still of working age. They can be used for longer-term leave (sabbaticals) as well as for further education, or family time with full pay. In the case of age-related long-term accounts, the intention is to withdraw the credits at the end of the individual’s working life. This makes early retirement or partial retirement possible without state funding.

Between 2002 and 2016, the intended use of long-term accounts has shifted (see Figure 2). In most businesses, the majority of accumulated time credits are intended to be used for sabbaticals. Second, they can be used for family-leave, the category with the strongest increase. In just over one in three companies with long-term accounts the credits can be used for further training periods, this trend also is rising. Interestingly, since 2002 the share of enterprises that offer early retirement as a means to balance the accumulated credit has decreased. Overall, businesses are increasingly offering their employees more choice as to how they use their time credits.

Conclusion

Our analyses show that working time accounts are still on the rise. They allow companies to adjust the labour input to short-term fluctuations in demand. Employees, on the other hand, can use the flexibility they offer in terms of working time to improve their work-life balance.

By contrast, the development of long-term accounts is stagnating at a consistently low level. The introduction of the Flexi II Act 2009 was intended to facilitate the use of working time flexibility over the course of a career. Overall, however, the hoped-for increase in respective company agreements did not occur, as can be seen in the data of the IAB Establishment Panel. The legal regulations are perceived as too complicated and are obviously not sufficiently attractive for employers who are the ones who ultimately decide on the introduction of such accounts.

From a worker’s point of view, long-term accounts could contribute to a flexible working life. However, any credit that is to be taken in the future must first be saved. A fundamental problem with this is that the benefits are realised in the long-term, while the costs are incurred directly in the form of decreased leisure time or unavailable income components. As a result, these options are usable for various groups of employees to varying degrees – depending on their occupational status, gender and family context. The time and financial capacity (or constraints) of large parts of the workforce are likely to make it difficult for many to put by a large amount of credit for the long term. In addition, some issues persist which have not been completely solved, such as when the employer changes.

In addition, long-term accounts compete with the short-term flexibility of employees – and, of course, of companies. Consistent saving for a longer-term goal is at the expense of time-flexibility in the present day. Additional hours worked on the long-term account are not available for short-term recreation – whether for errands, family commitments and undertakings or other interests. For companies, too, the expansion of long-term accounts would severely limit their responsiveness in periods of low demand, because employees would then hold the majority of their time credits in the long-term account, and cannot use them for short-term flexibility.

All in all, working time accounts are an important flexibility tool for both employees and employers. In times of increasing volatility and transformations in the world of work, the importance of flexible working hours is likely to increase further.

Literature

Balleer, Almut; Gehrke, Britta; Merkl, Christian (2017): Some surprising facts about working time accounts and the business cycle in Germany. In: International Journal of Manpower, Vol. 38, No. 7, pp. 940-953.

Burda, Michael C.; Hunt, Jennifer (2011): What explains the German labor market miracle in the Great Recession? In: Brookings Papers on Economic Activity, 42 (1), pp. 273–335.

Herzog-Stein, Alexander; Zapf, Ines (2014): Navigating the great recession: The impact of working time accounts in Germany. In: Industrial & Labor Relations Review, 67 (3), pp. 891–925.

Möller, Joachim (2010): The German labor market response in the world recession. De-mystifying a miracle. In: Journal for Labour Market Research, Vol. 47, No. 4, pp. 325–336.

Weber, Enzo (2015): The labour market in Germany: reforms, recession and robustness. In: De Economist, Vol. 163, No. 4, pp. 461–472.

Ellguth, Peter ; Gerner, Hans-Dieter; Zapf, Ines (2019): Working time accounts in the public- and private sector: flexible working hours are becoming increasingly important, In: IAB-Forum 11th of September 2019, https://www.iab-forum.de/en/working-time-accounts-in-the-public-and-private-sector-flexible-working-hours-are-becoming-increasingly-important/, Retrieved: 26th of April 2024

Since 1996 Peter Ellguth has been working as a senior researcher at the IAB.

Since 1996 Peter Ellguth has been working as a senior researcher at the IAB. Hans-Dieter Gerner is professor of “Quantitative Methods in Business and Economics” at Nuremberg Tech ( Technische Hochschule Nürnberg Georg Simon Ohm).

Hans-Dieter Gerner is professor of “Quantitative Methods in Business and Economics” at Nuremberg Tech ( Technische Hochschule Nürnberg Georg Simon Ohm). Dr Ines Zapf is a researcher in the department "Forecasts and Macroeconomic Analyses" at the IAB.

Dr Ines Zapf is a researcher in the department "Forecasts and Macroeconomic Analyses" at the IAB. Authors:

- Peter Ellguth

- Hans-Dieter Gerner

- Ines Zapf